The Trillion-Dollar Circularity: Why the AI IPO Wave Feels Like a Beautiful Trap

An analysis of the structural risks and circular capital loops defining the high-stakes AI IPO wave of 2026.

When Anthropic confidentially filed for its Initial Public Offering (IPO) on June 1, 2026, it did not just signal the arrival of another mega-cap tech stock. It set off an existential stress test for the entire global financial apparatus. Fresh off a staggering Series H round that raised $65 billion and pegged its post-money valuation at $965 billion, Anthropic is knocking on the public market's door at a size that eclipses almost every legacy enterprise on Earth.

But as we peer past the astronomical valuations of this impending IPO wave—which includes SpaceX’s targeted June 2026 public debut at up to $1.8 trillion—a deeply unsettling pattern emerges. This is not a standard capital-raising cycle. It is a highly insulated, self-referential capital carousel that looks increasingly like a beautiful, multi-trillion-dollar trap.

The Closed-Loop Economy of AI Giants

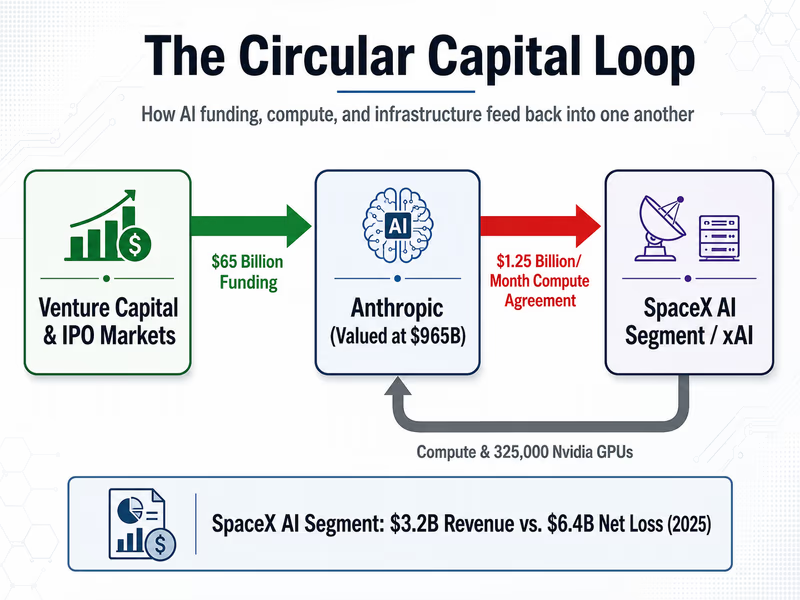

To understand the structural fragility of the current AI boom, one must look at the balance sheets, not the marketing decks. Consider the staggering agreement between SpaceX and Anthropic: SpaceX provides Anthropic with computing capacity—powered by approximately 325,000 Nvidia chips—at an eye-watering cost of $1.25 billion per month through May 2029.

On paper, this is a massive commercial contract. But look closer at the cash flow. In February 2026, SpaceX acquired xAI, directly entering the frontier LLM development race. Meanwhile, SpaceX's AI segment generated $3.2 billion in revenue in 2025 but posted a massive $6.4 billion loss, driven by aggressive R&D and capital expenditures. Anthropic's multi-billion dollar compute payments are effectively funding the infrastructure of a direct competitor, while Anthropic itself relies on massive capital injections—like its $65 billion Series H—to pay that very bill.

This is the definition of a circular investment economy. Private capital flows into Anthropic; Anthropic immediately funnels that cash to SpaceX/xAI for silicon access; SpaceX uses those revenues to offset its astronomical capital expenditures and R&D losses, inflating its own valuation to $1.8 trillion ahead of its public listing. When cash merely rotates within a closed ecosystem of mega-cap players, the valuations cease to reflect external market demand. Instead, they reflect the size of the pipeline connecting them.

The Venture Capital Distortion and the Pre-IPO Bubble

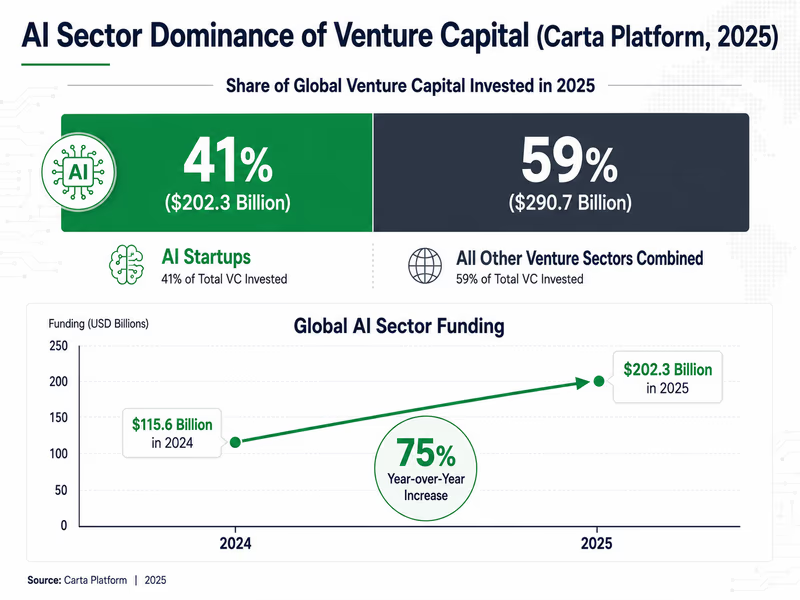

While public market bulls point to Nvidia’s solid earnings as proof of a healthy market, the private markets are displaying classic signs of late-stage mania. In 2025, AI startups captured a historic 41% of all venture dollars on the Carta platform, drawing in $202.3 billion globally—a 75% increase year-over-year.

When almost half of all global venture capital is concentrated in a single, unproven sector, price discovery breaks down entirely. Look no further than Cognition, an AI software engineering startup that raised $1 billion in a Series D round on June 5, 2026, valuing the tiny firm at $26 billion. Cognition’s CEO, Scott Wu, envisions a future where "software engineers operate more like architects, creatively structuring problems for armies of Devins to reliably execute on."

That vision is compelling, but the valuation is detached from current economic reality. As Ben Charoenwong, Associate Professor of Finance at INSEAD, warns: "I think the bubble is less in the listed market and more in pre-IPO AI start-ups. Many early-stage investors, including venture capitalists, will lose money if they continue pouring capital into loss-making, cash-burning AI start-ups with no clear path to profitability."

Without a massive, highly profitable enterprise adoption wave to absorb these systems, these startups are merely burning cash to buy chips, hoping that public market investors will bail them out at the IPO gate.

The Magnificent 7 and the Concentrated Market Risk

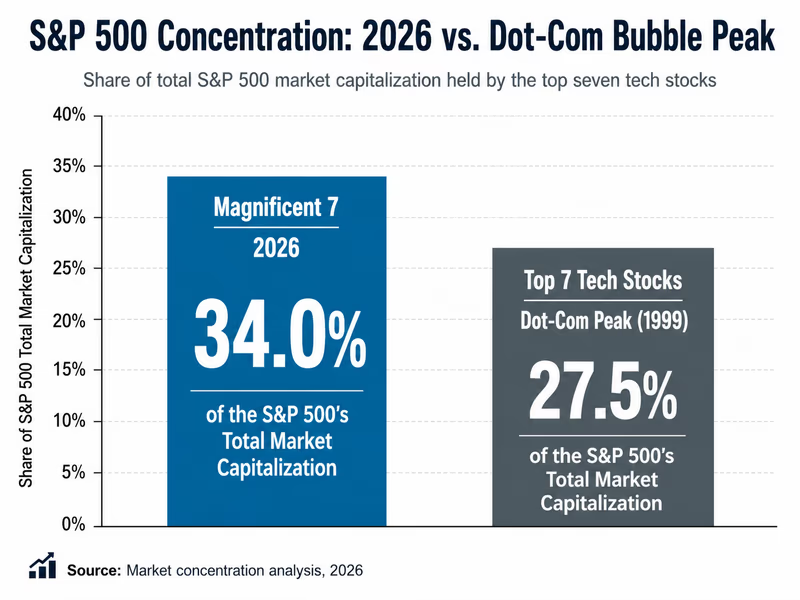

The systemic risk of this dynamic cannot be overstated. The "Magnificent 7" tech stocks now account for over 34% of the S&P 500's total market capitalization. This concentration matches, and in some metrics exceeds, the peak of the dot-com bubble in 1999.

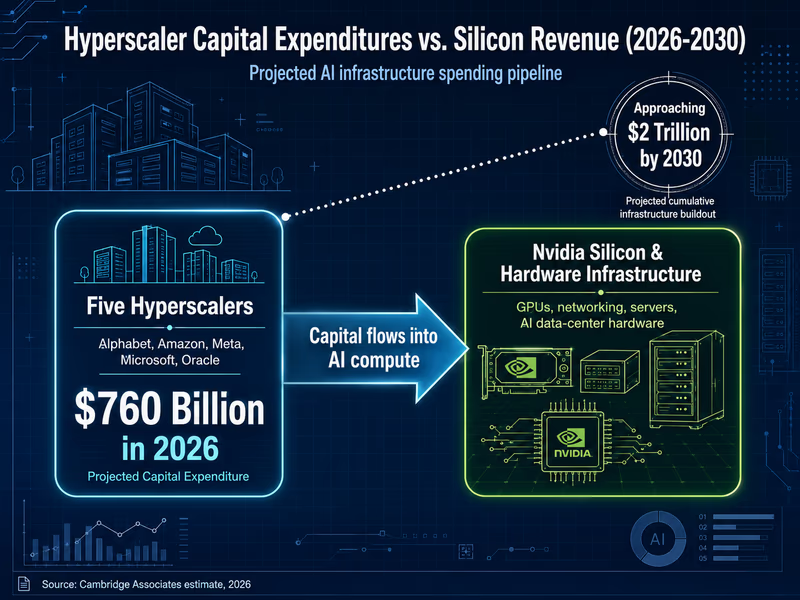

Back then, companies like Cisco and WorldCom built massive physical fiber-optic networks that lay dark for years because the consumer applications had not yet caught up to the bandwidth. Today, we are seeing a parallel infrastructure overbuild. The total capital expenditure for five major hyperscalers—Alphabet, Amazon, Meta, Microsoft, and Oracle—is estimated to hit $760 billion in 2026 alone, with projections nearing $2 trillion by 2030.

Where does this capital go? A significant portion flows straight to Nvidia, which reached a historic $2 trillion market capitalization on March 1, 2024. But as Jamie Dimon, CEO of JPMorgan Chase, astutely noted: "AI is real, but I think some money invested now will be wasted." If the enterprise revenue generated by these massive systems fails to cover the $760 billion annual depreciation of the hardware, the write-downs will be historic.

What This Means for Enterprises and Developers

For enterprise buyers, developers, and tech executives, the message is clear: do not build your business model on the assumption that frontier AI compute will remain subsidized by venture capital forever.

Currently, enterprise generative AI spending is surging, reaching $37 billion in 2025, up from $11.5 billion in 2024. However, much of this spending is experimental. If the public markets demand profitability from Anthropic and its peers post-IPO—as Harrison Rolfes of Pitchbook notes: "The AI company's profit margin will be a crucial indicator for the health of the wider AI boom"—these LLM providers will be forced to raise API pricing, cut back on free tiers, and rationalize their compute usage.

Businesses must prepare for a shift from cheap, subsidized experimentation to hard-nosed ROI calculations. If you cannot prove that an AI tool saves more in labor or infrastructure than its API costs, it will be cut from the budget.

The Coming Reckoning

The upcoming public listings of SpaceX and Anthropic—and the rumored September 2026 OpenAI IPO targeting an $852 billion valuation—will be the ultimate arbiters of the AI era. If these companies can show a clear path to high-margin profitability that does not rely on circular infrastructure deals, the boom will be vindicated, paving the way for what Federal Reserve Governor Lisa Cook calls "the most significant reorganization of the labor market."

But if their financial disclosures reveal that their revenues are merely recycled venture dollars spent on ever-increasing GPU bills, the valuation correction will be swift, severe, and systemic. The public markets have a brutal way of popping beautiful illusions. The AI sector is about to find out if it is built on solid ground, or merely floating on a cloud of highly valued promises.